Let’s visit a couple of fun and extremely counterintuitive problems which sit in the same family. The first appears to be a “paradox,” and illustrates a subtle fallacy. The second is an absolutely astonishing (and legitimate) algorithm for achieving better than 50-50 oods of picking the higher of two unknown envelopes. Plenty of articles have discussed who discovered what ad nauseum so we’ll just dive into the problems.

— The Two Envelope Paradox: Optimizing Expected Return —

First, consider the following scenario. Suppose you are shown two identical envelopes, each containing some amount of money unknown to you. You are told that one contains double the money in the other (but not which is which or what the amounts are) and are instructed to choose one. The one you select is placed in front of you and its contents are revealed. You then are given a second choice: keep it or switch envelopes. You will receive the amount in the envelope you choose. Your goal is to maximize your expected payment.

Our intuition tells us that no information has been provided by opening the envelope. After all, we didn’t know the two values beforehand so learning one of them tells us nothing. The probability of picking the higher envelope should be  regardless of whether we switch or not. But you weren’t asked to improve on the probability, just to maximize your expected payment. Consider the following 3 arguments:

regardless of whether we switch or not. But you weren’t asked to improve on the probability, just to maximize your expected payment. Consider the following 3 arguments:

- Let the amount in the the envelope you initially chose be

. If it is wrong to switch then the other envelope contains

. If it is wrong to switch then the other envelope contains  , but if it is right to switch it contains

, but if it is right to switch it contains  . There are even odds of either, so your expectation if you switch is

. There are even odds of either, so your expectation if you switch is  . This is better than the you get by sticking with the initial envelope, so it always is better to switch!

. This is better than the you get by sticking with the initial envelope, so it always is better to switch! - Since we don’t know anything about the numbers involved, opening the first envelope gives us no information — so ignore that value. Call the amount in the other envelope

. If it is wrong to switch then the envelope you chose contains

. If it is wrong to switch then the envelope you chose contains  , and if right to switch it contains

, and if right to switch it contains  . If you switch, you get but if you don’t your expectation is

. If you switch, you get but if you don’t your expectation is  . So it always is better NOT to switch!

. So it always is better NOT to switch! - Call the amounts in the two envelopes

and

and  (though you don’t know which envelope contains which). You pick one, but there is equal probability of it being either or . The expected reward thus is

(though you don’t know which envelope contains which). You pick one, but there is equal probability of it being either or . The expected reward thus is  . If you switch, the same holds true for the other envelope. So you still have an expected reward of . It doesn’t matter what you do.

. If you switch, the same holds true for the other envelope. So you still have an expected reward of . It doesn’t matter what you do.

Obviously, something is wrong with our logic. One thing that is clear is that we’re mixing apples and oranges with these arguments. Let’s be a bit more consistent with our terminology. Let’s call the value that is in the opened envelope and the values in the two envelopes and . We don’t know which envelope contains each, though. When we choose the first envelope, we observe a value . This value may be or .

In the 3rd argument,  . If we switch, then

. If we switch, then  . If we keep the initial envelope then

. If we keep the initial envelope then  . Whether we switch or not, the expected value is though we do not know what this actually is. It could correspond to

. Whether we switch or not, the expected value is though we do not know what this actually is. It could correspond to  or

or  . We must now draw an important distinction. It is correct that for the known and given our definition of as the minimum of the two envelopes. However, we cannot claim that is or with equal probability! That would be tantanmount to claiming that the envelopes contain the pairs

. We must now draw an important distinction. It is correct that for the known and given our definition of as the minimum of the two envelopes. However, we cannot claim that is or with equal probability! That would be tantanmount to claiming that the envelopes contain the pairs  or

or  with equal probability. We defined to be the minimum value so the first equality holds, but we would need to impose a constraint on the distribution over that minimum value itself in order for the second one to hold. This is a subtle point and we will return to it shortly. Suffice it to say that if we assume such a thing we are led right to the same fallacy the first two arguments are guilty of.

with equal probability. We defined to be the minimum value so the first equality holds, but we would need to impose a constraint on the distribution over that minimum value itself in order for the second one to hold. This is a subtle point and we will return to it shortly. Suffice it to say that if we assume such a thing we are led right to the same fallacy the first two arguments are guilty of.

Obviously, the first two arguments can’t both be correct. Their logic is the same and therefore they must both be wrong. But how? Before describing the problems, let’s consider a slight variant in which you are NOT shown the contents of the first envelope before being asked to switch. It may seem strange that right after you’ve chosen, you are given the option to switch when no additional information has been presented. Well, this really is the same problem. With no apriori knowledge of the distribution over , it is immaterial whether the first envelope is opened or not before the 2nd choice is made. This gives us a hint as to what is wrong with the first two arguments.

There actually are two probability distributions at work here, and we are confounding them. The first is the underlying distribution on ordered pairs or, equivalently, the distribution of the lower element . Let us call it  . It determines which two numbers

. It determines which two numbers  we are dealing with. We do not know .

we are dealing with. We do not know .

The second relevant distribution is over how two given numbers (in our case ) are deposited in the envelopes (or equivalently, how the player orders the envelopes by choosing one first). This distribution unambiguously is 50-50.

The problem arises when we implicitly assume a form for or attempt to infer information about it from the revealed value . Without apriori knowledge of , being shown makes no difference at all. Arguments which rely solely on the even-odds of the second distribution are fine, but arguments which implicitly involve run into trouble.

The first two arguments make precisely this sort of claim. They implicitly assume that the pairs or can occur with equal probability. Suppose they couldn’t. For simplicity (and without reducing the generality of the problem), let’s assume that the possible values in the envelopes are constrained to  with

with  . The envelopes thus contain

. The envelopes thus contain  for some integer

for some integer  (though we don’t know which envelope contains which value). For convenience, let’s work in terms of

(though we don’t know which envelope contains which value). For convenience, let’s work in terms of  of the values involved (taking care to use when computing expectations).

of the values involved (taking care to use when computing expectations).

In these terms, the two envelopes contain  for some

for some  (defined to be the lesser of the two). We open one, and see

(defined to be the lesser of the two). We open one, and see  . If it is the upper then the pair is

. If it is the upper then the pair is  , otherwise the pair is

, otherwise the pair is  . To claim that these have equal probabilities means that

. To claim that these have equal probabilities means that  and

and  are equally probable. We made this assumption independent of the value of

are equally probable. We made this assumption independent of the value of  , so it would require that all pairs be equally probable.

, so it would require that all pairs be equally probable.

So what? Why not just assume a uniform distribution? Well, for one thing, we should be suspicious that we require an assumption about . The 3rd argument requires no such assumption. Even if we were to assume a form for , we can’t assume it is uniform. Not just can’t as in “shouldn’t”, but can’t as in “mathematically impossible.” It is not possible to construct a uniform distribution on  .

.

Suppose we sought to circumvent this issue by constraining ourselves to some finite range ![{[M,N]}](https://s0.wp.com/latex.php?latex=%7B%5BM%2CN%5D%7D&bg=fefeeb&fg=000000&s=0&c=20201002) , which we supposedly know or assume apriori. We certainly can impose a uniform distribution on it. Each pair has probability

, which we supposedly know or assume apriori. We certainly can impose a uniform distribution on it. Each pair has probability  with

with ![{n\in [M,N-1]}](https://s0.wp.com/latex.php?latex=%7Bn%5Cin+%5BM%2CN-1%5D%7D&bg=fefeeb&fg=000000&s=0&c=20201002) . But now we’ve introduced additional information (in the form of

. But now we’ve introduced additional information (in the form of  and

and  ), and it no longer is surprising that we can do better than even-odds! We always would switch unless the first envelope contained . There is no contradiction between the first two arguments because we have apriori knowledge and are acting on it. We no longer are true to the original game.

), and it no longer is surprising that we can do better than even-odds! We always would switch unless the first envelope contained . There is no contradiction between the first two arguments because we have apriori knowledge and are acting on it. We no longer are true to the original game.

Rather than dwell on this particular case, let’s solve the more general case of a given (or in terms of ,  ). For any drawn according to , the envelopes contain in some order and it is equally likely that

). For any drawn according to , the envelopes contain in some order and it is equally likely that  and

and  . If we know

. If we know  we can bet accordingly since it contains information. In that case, knowing (i.e. ) helps us. Let’s suppose we don’t know . Then it still does not matter whether we observe the value , because we don’t the know the underlying distribution!

we can bet accordingly since it contains information. In that case, knowing (i.e. ) helps us. Let’s suppose we don’t know . Then it still does not matter whether we observe the value , because we don’t the know the underlying distribution!

There only are two deterministic strategies: always keep, always switch. Why? Suppose that the drawn value is (unknown to us) and the observed value is . Note that these don’t require actual knowledge of the value, just that it has been fixed by the process of opening the envelope. Since we don’t know the underlying distribution, our strategy will be independent of the actual value. Given that the value doesn’t matter, we have nothing to do but always keep or always switch.

First consider the expected value with the always-keep strategy:

![\displaystyle \langle V_K \rangle= \sum_{n=-\infty}^\infty P(n) [P(m=n|n) 2^n + P(m=n+1|n) 2^{n+1}]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Clangle+V_K+%5Crangle%3D+%5Csum_%7Bn%3D-%5Cinfty%7D%5E%5Cinfty+P%28n%29+%5BP%28m%3Dn%7Cn%29+2%5En+%2B+P%28m%3Dn%2B1%7Cn%29+2%5E%7Bn%2B1%7D%5D&bg=fefeeb&fg=000000&s=0&c=20201002)

I.e. we sum over all possible ordered pairs and then allow equal probability  for either of the two envelope orders. So we have

for either of the two envelope orders. So we have  . We immediately see that for this to be defined the probability distribution must drop faster than as gets large! We already have a constraint on the possible forms for .

. We immediately see that for this to be defined the probability distribution must drop faster than as gets large! We already have a constraint on the possible forms for .

Next consider the always-switch strategy. It’s easy to see that we get the same result:

![\displaystyle \langle V_S \rangle= \sum_{n=-\infty}^\infty P(n) [P(m=n|n) 2^{n+1} + P(m=n+1|n) 2^{n}]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Clangle+V_S+%5Crangle%3D+%5Csum_%7Bn%3D-%5Cinfty%7D%5E%5Cinfty+P%28n%29+%5BP%28m%3Dn%7Cn%29+2%5E%7Bn%2B1%7D+%2B+P%28m%3Dn%2B1%7Cn%29+2%5E%7Bn%7D%5D&bg=fefeeb&fg=000000&s=0&c=20201002)

and since  we get the same answer.

we get the same answer.

But let’s be extra pedantic, and connect this to the original formulation of the first two arguments. I.e., we should do it in terms of , the observed value.

![\displaystyle \langle V_S \rangle= \sum_m P(m) [P(n=m|m) 2^{m+1} + P(n=m-1|m) 2^{m-1}]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Clangle+V_S+%5Crangle%3D+%5Csum_m+P%28m%29+%5BP%28n%3Dm%7Cm%29+2%5E%7Bm%2B1%7D+%2B+P%28n%3Dm-1%7Cm%29+2%5E%7Bm-1%7D%5D&bg=fefeeb&fg=000000&s=0&c=20201002)

We observe that  and

and  . We know that

. We know that  . Plugging these in, we get

. Plugging these in, we get

![\displaystyle \langle V_S \rangle= \sum_m [0.5 P(n=m) 2^{m+1} + 0.5 P(n=m-1) 2^{m-1}]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Clangle+V_S+%5Crangle%3D+%5Csum_m+%5B0.5+P%28n%3Dm%29+2%5E%7Bm%2B1%7D+%2B+0.5+P%28n%3Dm-1%29+2%5E%7Bm-1%7D%5D&bg=fefeeb&fg=000000&s=0&c=20201002)

The first term gives us  . We can rewrite the index on the 2nd sum to get

. We can rewrite the index on the 2nd sum to get  , which gives us

, which gives us  , the exact same expression as before!

, the exact same expression as before!

How does this apply to the ranged example we gave before? When we discussed it, we considered the case where the underlying distribution was known. In that and all other cases, a better than even-odds strategy based on such knowledge can be computed. In our actual formulation of the game, we don’t know and there’s no reason it couldn’t be uniform on some unknown interval . Suppose it was. It still seems from our earlier discussion as if we’d do better by always switching. We don’t. The average amount thrown away by incorrectly switching when  exactly offsets the average gain from switching in all other cases. We do no better by switching than by keeping.

exactly offsets the average gain from switching in all other cases. We do no better by switching than by keeping.

We thus see that without knowing the underlying distribution , the switching and keeping strategies have the same expected reward. Of the three arguments we originally proposed, the first 2 were flawed in that they assume a particular, and impossible, underlying distribution for .

At the beginning of our discussion, we mentioned that our intuition says you cannot do better than 50-50 probability-wise. Let us set aside expected rewards and focus solely on probabilities. We now see how you actually can do better than 50-50, contrary to all intuition!

— Achieving better than 50-50 Odds with Two Envelopes —

Next let’s consider a broader class of two-envelope problems, but purely from the standpoint of probabilities. Now the two envelopes can contain any numbers; one need not be double the other. As before, we may choose an envelope, it is opened, and we are offered the opportunity to keep it or switch. Unlike before, our goal now is to maximize the probability of picking the larger envelope.

Since we are dealing with probabilities rather than expectation values, we don’t care what two numbers the envelopes contain. In fact, they need not be numbers at all — as long as they are distinct and comparable (i.e.  or

or  but not both). To meaningfully analyze the problem we require a slightly stronger assumption, though: specifically that the set from which they be drawn (without repetition) possesses a strict linear ordering. However, it need not even possess any algebraic structure or a metric. Since we are not concerned with expectation values, no such additional structure is necessary.

but not both). To meaningfully analyze the problem we require a slightly stronger assumption, though: specifically that the set from which they be drawn (without repetition) possesses a strict linear ordering. However, it need not even possess any algebraic structure or a metric. Since we are not concerned with expectation values, no such additional structure is necessary.

Our intuition immediately tells us that nothing can be gained by switching. In fact, nothing we do should have any impact on the outcome. After all, the probability of initially picking correctly is . Switching adds no information and lands us with an identical probability. And that is that, right? It turns out that, contrary to our very strong intuition about the problem, there is in fact a way to improve those odds. To accomplish this, we’ll need to introduce a source of randomness. For convenience of exposition we’ll assume the envelopes contain real numbers, and revisit the degree to which we can generalize the approach later.

The procedure is as follows:

- Pick any continuous probability distribution which has support on all of

(i.e.

(i.e.  for all real ). Most common distributions (normal, beta, exponential, etc) are fine.

for all real ). Most common distributions (normal, beta, exponential, etc) are fine. - Choose an envelope and open it. We’ll denote its value .

- Sample some value

from our distribution . If

from our distribution . If  stick with the initial choice, otherwise switch. We’ll refer to or

stick with the initial choice, otherwise switch. We’ll refer to or  because the probability that

because the probability that  has measure

has measure  and safely can be ignored.

and safely can be ignored.

At first, second, and  glance, this seems pointless. It feels like all we’ve done is introduce a lot of cruft which will have no effect. We can go stand in a corner flipping a coin, play Baccarat at the local casino, cast the bones, or anything else we want, and none of that can change the probability that we’re equally likely to pick the lower envelope as the higher one initially — and thus equally likely to lose as to gain by switching. With no new information, there can be no improvement. Well, let’s hold that thought and do the calculation anyway. Just for fun.

glance, this seems pointless. It feels like all we’ve done is introduce a lot of cruft which will have no effect. We can go stand in a corner flipping a coin, play Baccarat at the local casino, cast the bones, or anything else we want, and none of that can change the probability that we’re equally likely to pick the lower envelope as the higher one initially — and thus equally likely to lose as to gain by switching. With no new information, there can be no improvement. Well, let’s hold that thought and do the calculation anyway. Just for fun.

First some terminology. We’ll call the value in the opened envelope , and the value in the other envelope . The decision we must make is whether to keep or switch to the unknown . We’ll denote by and  the values in the two envelopes in order. I.e.,

the values in the two envelopes in order. I.e.,  by definition. In terms of and we have

by definition. In terms of and we have  and

and  . We’ll denote our contrived distribution in the abstract, with pdf

. We’ll denote our contrived distribution in the abstract, with pdf  and cdf

and cdf  .

.

Let’s examine the problem from a Bayesian perspective. There is a 50-50 chance that  or

or  . So

. So  . There are no subtleties lurking here. We’ve assumed nothing about the underlying distribution over

. There are no subtleties lurking here. We’ve assumed nothing about the underlying distribution over  . Whatever the envelopes contain, we are equally likely to initially pick the one with or the one with .

. Whatever the envelopes contain, we are equally likely to initially pick the one with or the one with .

Once the initial envelope has been opened, and the value revealed, we sample from our selected distribution and clearly have  and

and  and

and  . The latter forms the criterion by which we will keep or switch to . Please note that in what follows, is not a free variable, but rather a mere notational convenience. Something like

. The latter forms the criterion by which we will keep or switch to . Please note that in what follows, is not a free variable, but rather a mere notational convenience. Something like  is just notation for “the probability the sampled value is greater than .” We can apply Bayes’ law to get (with all probabilities conditional on some unknown choice of ):

is just notation for “the probability the sampled value is greater than .” We can apply Bayes’ law to get (with all probabilities conditional on some unknown choice of ):

What we really care about is the ratio:

Here, we’ve observed that  and

and  since by assumption and

since by assumption and  is monotonically increasing (we assumed its support is all of ). I.e., if

is monotonically increasing (we assumed its support is all of ). I.e., if  there is a greater probability that

there is a greater probability that  than

than  . We shouldn’t switch. A similar argument shows we should switch if

. We shouldn’t switch. A similar argument shows we should switch if  .

.

So what the heck has happened, and where did the new information come from? What happened is that we actually know one piece of information we had not used: that the interval has nonzero probability measure. I.e. there is some “space” between and . We don’t know the underlying distribution but we can pretend we do. Our strategy will be worse than if we did know the underlying  , of course. We’ll return to this shortly, but first let’s revisit the assumptions which make this work. We don’t need the envelopes to contain real numbers, but we do require the following of the values in the envelopes:

, of course. We’ll return to this shortly, but first let’s revisit the assumptions which make this work. We don’t need the envelopes to contain real numbers, but we do require the following of the values in the envelopes:

- The set of possible values forms a measurable set with a strict linear ordering.

- Between any two elements there is a volume with nonzero probability. Actually, this only is necessary if we require a nonzero improvement for any . If we only require an improvement on average we don’t need it. But in that scenario, the host can contrive to use a distribution which neutralizes our strategy and returns us to 50-50 odds.

What difference does itself make? We don’t have any way to choose an “optimal” distribution because that would require placing the bulk of probability where we think and are likely to lie. I.e. we would require prior knowledge. All we can guarantee is that we can improve things by some (perhaps tiny) amount. We’ll compute how much (for a given true underlying distribution) shortly.

Let’s assume that  is the true underlying distribution over . We won’t delve into what it means to “know”

is the true underlying distribution over . We won’t delve into what it means to “know”  since we are handed the envelopes to begin with. Perhaps the game is played many times with values drawn according to or maybe it is a one-time affair with fixed (i.e. a

since we are handed the envelopes to begin with. Perhaps the game is played many times with values drawn according to or maybe it is a one-time affair with fixed (i.e. a  -distribution). Ultimately, such considerations just would divert us to the standard core philosophical questions of probability theory. Suffice to say that there exists some . By definition

-distribution). Ultimately, such considerations just would divert us to the standard core philosophical questions of probability theory. Suffice to say that there exists some . By definition  unless . For convenience, we’ll define a symmetrized version as well:

unless . For convenience, we’ll define a symmetrized version as well:  . We don’t employ a factor of since the two terms are nonzero on disjoint domains.

. We don’t employ a factor of since the two terms are nonzero on disjoint domains.

Given , what gain do we get from a particular choice of ?

![\displaystyle \begin{array}{rcl} P(win)= \int_{x<y} dx dy Q(x,y)[p(z=x|(x,y))p(x<d) \\ + p(z=y|(x,y))p(d<y)] \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cbegin%7Barray%7D%7Brcl%7D++P%28win%29%3D+%5Cint_%7Bx%3Cy%7D+dx+dy+Q%28x%2Cy%29%5Bp%28z%3Dx%7C%28x%2Cy%29%29p%28x%3Cd%29+%5C%5C+%2B+p%28z%3Dy%7C%28x%2Cy%29%29p%28d%3Cy%29%5D+%5Cend%7Barray%7D+&bg=fefeeb&fg=000000&s=0&c=20201002)

I.e., the probability we keep when it is and switch when it is . Clearly,  since those are the immutable 50-50 envelope ordering probabilities. After a little rearrangement, we get:

since those are the immutable 50-50 envelope ordering probabilities. After a little rearrangement, we get:

Our gain is the mean value of  over the joint distribution . The more probability jams between and , the more we gain should that arise. But without knowledge of the underlying joint distribution , we have no idea how best to pick . All we can do is guarantee some improvement.

over the joint distribution . The more probability jams between and , the more we gain should that arise. But without knowledge of the underlying joint distribution , we have no idea how best to pick . All we can do is guarantee some improvement.

How well can we do if we actually know ? Well, there are two ways to use such information. We could stick to our strategy and try to pick an optimal , or we could seek to use knowledge of directly. In order to do the former, we need to exercise a little care. is a two-dimensional distribution while is one-dimensional. How would we use to pick ? Well, this is where we make use of the observed .

In our previous discussion of the envelope switching fallacy, the value of turned out to be a red-herring. Here it is not. Observing is essential here, but only for computation of probabilities. As mentioned, we assume no algebraic properties and are computing no expectations. We already know that the observation of is critical, since our algorithm pivots on a comparison between and our randomly sampled value . Considering our ultimate goal (keep or switch), it is clear what we need from : a conditional probability that  . However, we cannot directly use

. However, we cannot directly use  because we defined . We want

because we defined . We want  and we don’t know whether

and we don’t know whether  or

or  . Let’s start by computing the probability of (being the observed value) and of

. Let’s start by computing the probability of (being the observed value) and of  (being the observed and unobserved values).

(being the observed and unobserved values).

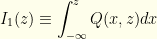

The probability of observing and the other envelope having is the probability that the relevant ordered pair was chosen for the two envelopes multiplied by the probability that we initially opened the envelop containing the value corresponding to our observed rather than the other one.

To get  we integrate this.

we integrate this.  . This is a good point to introduce two quantities which will be quite useful going forward.

. This is a good point to introduce two quantities which will be quite useful going forward.

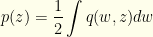

In terms of these,

![\displaystyle p(z)= \frac{1}{2}[I_1(z)+I_2(z)]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+p%28z%29%3D+%5Cfrac%7B1%7D%7B2%7D%5BI_1%28z%29%2BI_2%28z%29%5D&bg=fefeeb&fg=000000&s=0&c=20201002)

There’s nothing special about calling the variables or in the integrals and it is easy to see (since each only covers half the domain) that we get what we would expect:

What we want is the distribution  . This gives us:

. This gives us:

Finally, this gives us the desired quantity  . It is easy to see that:

. It is easy to see that:

As an example, consider the previous case — where one envelope holds twice what the other does. We observe , and must be either or , though we don’t know with what probabilities. If we are given the underlying distribution on , say  , we can figure that out.

, we can figure that out.  and

and  is the symmetrized version.

is the symmetrized version. ![{\int q(w,z)dw= \int dw [Q(w,z)+Q(z,w)]= (P_2(z/2)+P_2(2z))}](https://s0.wp.com/latex.php?latex=%7B%5Cint+q%28w%2Cz%29dw%3D+%5Cint+dw+%5BQ%28w%2Cz%29%2BQ%28z%2Cw%29%5D%3D+%28P_2%28z%2F2%29%2BP_2%282z%29%29%7D&bg=fefeeb&fg=000000&s=0&c=20201002) . So

. So  . This is just what we’d expect — though we’re really dealing with discrete values and are being sloppy (which ends us up with a ratio of infinities from the function when computing probability ratios, but we’ll ignore that here). The relevant probability ratio clearly is

. This is just what we’d expect — though we’re really dealing with discrete values and are being sloppy (which ends us up with a ratio of infinities from the function when computing probability ratios, but we’ll ignore that here). The relevant probability ratio clearly is  . From a purely probability standpoint, we should switch if

. From a purely probability standpoint, we should switch if  . If we reimpose the algebraic structure and try to compute expectations (as in the previous problem) we would get an expected value of from keeping and an expected value of

. If we reimpose the algebraic structure and try to compute expectations (as in the previous problem) we would get an expected value of from keeping and an expected value of ![{z[P_2(z/2)/2 + 2P(2z)]}](https://s0.wp.com/latex.php?latex=%7Bz%5BP_2%28z%2F2%29%2F2+%2B+2P%282z%29%5D%7D&bg=fefeeb&fg=000000&s=0&c=20201002) from switching . Whether this is less than or greater than depends on the distribution

from switching . Whether this is less than or greater than depends on the distribution  .

.

Returning to our analysis, let’s see how often we are right about switching if we know the actual distribution and use that knowledge directly. The strategy is obvious. Using our above formulae, we can compute  directly. To optimize our probability of winning, we observe then we switch iff

directly. To optimize our probability of winning, we observe then we switch iff  . If there is additional algebraic structure and expectations can be defined, then an analogous calculations give whatever switching criterion maximizes the relevant expectation value.

. If there is additional algebraic structure and expectations can be defined, then an analogous calculations give whatever switching criterion maximizes the relevant expectation value.

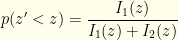

In terms of probabilities, full knowledge of is the best we can do. The probability we act correctly is:

![\displaystyle \begin{array}{rcl} P'(win)= \int dz \frac{[\theta(I_1(z)-I_2(z)) I_1(z) + \theta(I_2(z)-I_1(z))I_2(z)]}{I_1(z)+I_2(z)} \\ = \int dz \frac{\max(I_1(z),I_2(z))}{(I_1(z)+I_2(z)} \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cbegin%7Barray%7D%7Brcl%7D++P%27%28win%29%3D+%5Cint+dz+%5Cfrac%7B%5B%5Ctheta%28I_1%28z%29-I_2%28z%29%29+I_1%28z%29+%2B+%5Ctheta%28I_2%28z%29-I_1%28z%29%29I_2%28z%29%5D%7D%7BI_1%28z%29%2BI_2%28z%29%7D+%5C%5C+%3D+%5Cint+dz+%5Cfrac%7B%5Cmax%28I_1%28z%29%2CI_2%28z%29%29%7D%7B%28I_1%28z%29%2BI_2%28z%29%7D+%5Cend%7Barray%7D+&bg=fefeeb&fg=000000&s=0&c=20201002)

Since  and

and  are monotonic (one increasing, the other decreasing), we have a cutoff value

are monotonic (one increasing, the other decreasing), we have a cutoff value  (defined by

(defined by  ) below which we should switch and above which we should not.

) below which we should switch and above which we should not.

How do we do with our invented instead? We could recast our earlier formula for  into our current notation, but it’s easier to compute directly. For given , the actual probability of needing to switch is

into our current notation, but it’s easier to compute directly. For given , the actual probability of needing to switch is  . Based on our algorithm, we will do so with probability

. Based on our algorithm, we will do so with probability  . The probability of not needing to switch is

. The probability of not needing to switch is  and we do so with probability

and we do so with probability  . I.e., our probability of success for given is:

. I.e., our probability of success for given is:

For any given , this is of the form  where

where  and

and  . The optimal solutions lie at one end or the other. So it obviously is best to have

. The optimal solutions lie at one end or the other. So it obviously is best to have  when

when  and

and  when

when  . This would be discontinuous, but we could come up with a smoothed step function (ex. a logistic function) which is differentiable but arbitrarily sharp. The gist is that we want all the probability in concentrated around . Unfortunately, we have no idea where is!

. This would be discontinuous, but we could come up with a smoothed step function (ex. a logistic function) which is differentiable but arbitrarily sharp. The gist is that we want all the probability in concentrated around . Unfortunately, we have no idea where is!

Out of curiosity, what if we pick instead to be the conditional distribution itself once we’ve observed ? We’ll necessarily do worse than by direct comparison using (the max formula above), but how much worse? Well,  . Integrating over we have

. Integrating over we have  . I.e., We end up with

. I.e., We end up with  as our probability of success. If we had used

as our probability of success. If we had used  for our instead we would get

for our instead we would get  instead. Neither is optimal in general.

instead. Neither is optimal in general.

Next, let’s look at the problem from an information theory standpoint. As mentioned, there are two sources of entropy: (1) the choice of the underlying pair (with by definition) and (2) the selection or determined by our initial choice of an envelope. The latter is a fair coin toss with no information and maximum entropy. The information content of the former depends on the (true) underlying distribrution.

Suppose we have perfect knowledge of the underlying distribution. Then any given arises with probability ![{p(z)=\frac{1}{2}[I_1(z)+I_2(z)]}](https://s0.wp.com/latex.php?latex=%7Bp%28z%29%3D%5Cfrac%7B1%7D%7B2%7D%5BI_1%28z%29%2BI_2%28z%29%5D%7D&bg=fefeeb&fg=000000&s=0&c=20201002) . Given that , we have a Bernoulli random variable

. Given that , we have a Bernoulli random variable  given by . The entropy of that specific coin toss (i.e. the conditional entropy of the Bernoulli distribution

given by . The entropy of that specific coin toss (i.e. the conditional entropy of the Bernoulli distribution  ) is

) is

![\displaystyle H(z'>z|z)= \frac{-I_1(z)\ln I(z) - I_2(z)\ln I_2(z) + (I_1(z)+I_2(z))\ln [I_1(z)+I_2(z)]}{I_1(z)+I_2(z)}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+H%28z%27%3Ez%7Cz%29%3D+%5Cfrac%7B-I_1%28z%29%5Cln+I%28z%29+-+I_2%28z%29%5Cln+I_2%28z%29+%2B+%28I_1%28z%29%2BI_2%28z%29%29%5Cln+%5BI_1%28z%29%2BI_2%28z%29%5D%7D%7BI_1%28z%29%2BI_2%28z%29%7D&bg=fefeeb&fg=000000&s=0&c=20201002)

With our contrived distribution , we are implicitly are operating as if  . This yields a conditional entropy:

. This yields a conditional entropy:

There is a natural measure of the information cost of assuming an incorrect distribution. It is the Kullback Liebler Divergence (also known as the relative entropy). While it wouldn’t make sense to compute it between and (which are, among other things, of different dimension, we certainly can compare the cost for given of the difference in our Bernoulli random variables for switching — and then integrate over to get an average cost in bits. Let’s denote by  the probability based on the true distribution and keep for the contrived one. I.e.

the probability based on the true distribution and keep for the contrived one. I.e.  and . For given , the K-L divergence is:

and . For given , the K-L divergence is:

![\displaystyle D(Q || P, z)= \frac{-I_2(z)\ln [(I_1(z)+I_2(z))(1-F(z))/I_2(z)] - I_1(z)\ln [(I_1(z)+I_2(z))F(z)/I_1(z)]}{I_1(z)+I_2(z)}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+D%28Q+%7C%7C+P%2C+z%29%3D+%5Cfrac%7B-I_2%28z%29%5Cln+%5B%28I_1%28z%29%2BI_2%28z%29%29%281-F%28z%29%29%2FI_2%28z%29%5D+-+I_1%28z%29%5Cln+%5B%28I_1%28z%29%2BI_2%28z%29%29F%28z%29%2FI_1%28z%29%5D%7D%7BI_1%28z%29%2BI_2%28z%29%7D&bg=fefeeb&fg=000000&s=0&c=20201002)

Integrating this, we get the mean cost in bits of being wrong.

![\displaystyle \begin{array}{rcl} \langle D(Q || P) \rangle= \frac{1}{2}\int dz [-(I_1(z)+I_2(z))\ln [I_1(z)+I_2(z)] - I_2(z)\ln (1-F(z)) \\ -I_1(z)\ln F(z) + I_1(z)\ln I_1(z) + I_2(z)\ln I_2(z)] \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cbegin%7Barray%7D%7Brcl%7D++%5Clangle+D%28Q+%7C%7C+P%29+%5Crangle%3D+%5Cfrac%7B1%7D%7B2%7D%5Cint+dz+%5B-%28I_1%28z%29%2BI_2%28z%29%29%5Cln+%5BI_1%28z%29%2BI_2%28z%29%5D+-+I_2%28z%29%5Cln+%281-F%28z%29%29+%5C%5C+-I_1%28z%29%5Cln+F%28z%29+%2B+I_1%28z%29%5Cln+I_1%28z%29+%2B+I_2%28z%29%5Cln+I_2%28z%29%5D+%5Cend%7Barray%7D+&bg=fefeeb&fg=000000&s=0&c=20201002)

The first term is simply  , the entropy of our actual distribution over . In fact, the first term and last 2 terms together we recognize as

, the entropy of our actual distribution over . In fact, the first term and last 2 terms together we recognize as  , the mean Bernoulli entropy of the actual distribution. In these terms, we have:

, the mean Bernoulli entropy of the actual distribution. In these terms, we have:

where the expectations are over the unconditional actual distribution . The 2nd expectation on the right represents the cost of being wrong about . If it was the optimal distribution with all probability centered near then the term on the right would approach and there would be no entropy cost.

As an aside, this sort of probabilistic strategy should not be confused with the mixed strategies of game theory. In our case, a mixed strategy would be an apriori choice  where

where  is the always-keep strategy,

is the always-keep strategy,  is the always-switch strategy, and

is the always-switch strategy, and  is the probability of employing the always-keep strategy. A player would flip a biased-coin with Bernoulli probability

is the probability of employing the always-keep strategy. A player would flip a biased-coin with Bernoulli probability  and choose one of the two-strategies based on it. That has nothing to do with the measure-theory approach we’re taking here. In particular, a mixes strategy makes no use of the observed value or its relation to the randomly sampled value. Any mixed strategy gives even-odds because the two underlying deterministic strategies both have even-odds.

and choose one of the two-strategies based on it. That has nothing to do with the measure-theory approach we’re taking here. In particular, a mixes strategy makes no use of the observed value or its relation to the randomly sampled value. Any mixed strategy gives even-odds because the two underlying deterministic strategies both have even-odds.

over parameters

over parameters  (with state space

(with state space  ). We acquire some data

). We acquire some data  , and wish to use it to infer

, and wish to use it to infer  is easy to compute or sample, and (3) the normalization

is easy to compute or sample, and (3) the normalization  is not expensive to compute or adequately approximate.

is not expensive to compute or adequately approximate. . However, there also is another view we may take. We need not restrict ourselves to a single Bayesian update. It is perfectly reasonable to ask whether multiple updates using the same

. However, there also is another view we may take. We need not restrict ourselves to a single Bayesian update. It is perfectly reasonable to ask whether multiple updates using the same  . Our method is conceptually equivalent to performing successive experiments which happen to produce the same data

. Our method is conceptually equivalent to performing successive experiments which happen to produce the same data  is a derived normalization factor, nothing more.

is a derived normalization factor, nothing more. , and denote the elements of

, and denote the elements of  .

. -vectors to denote probability or conditional probability distributions over

-vectors to denote probability or conditional probability distributions over  component the probability of

component the probability of  ), but it turns out to be simpler to use diagonal

), but it turns out to be simpler to use diagonal  matrices.

matrices. with

with  .

. the data set

the data set  times. I.e., the equivalent of having performed an experiment

times. I.e., the equivalent of having performed an experiment  is an

is an  with

with  ).

). via an

via an  , with

, with  . Note that

. Note that  and

and  .

. with

with  .

. is a scalar. In our notation,

is a scalar. In our notation,  .

. . What happens if we repeat this? A second iteration substitutes

. What happens if we repeat this? A second iteration substitutes  . This is homogeneous of degree

. This is homogeneous of degree  in

in  normalization factor in

normalization factor in  . The same reasoning extends to

. The same reasoning extends to  .

. , and let

, and let  . Our expression for

. Our expression for  after

after  .

. , which can be written

, which can be written  . We know that

. We know that  , so as long as

, so as long as  we have

we have  . Specifically, for

. Specifically, for  we have

we have  for

for  . Note that the denominator is negative since

. Note that the denominator is negative since  and the numerator is negative for small enough

and the numerator is negative for small enough  .

. . If we perform the same analysis for

. If we perform the same analysis for  , we get

, we get  , which corresponds to

, which corresponds to  . The denominator diverges for large enough

. The denominator diverges for large enough  .

. . As

. As  , all but the dominant

, all but the dominant  are exponentially suppressed. The net effect of infinite iteration is to pick out the maximum likelihood value. I.e., we select the

are exponentially suppressed. The net effect of infinite iteration is to pick out the maximum likelihood value. I.e., we select the  for

for  and

and  . It is easy to see what happens in this case.

. It is easy to see what happens in this case.  , so

, so  and

and  . Note that

. Note that  here, but we stated the denominator explicitly to facilitate visualization of the extension to

here, but we stated the denominator explicitly to facilitate visualization of the extension to  degenerate maximum

degenerate maximum  (each

(each  ). The limit of iterated posteriors

). The limit of iterated posteriors  . This reduces to our previous result when

. This reduces to our previous result when  .

. for the maximum likelihood

for the maximum likelihood  ‘s from contention for the maximum likelihood.

‘s from contention for the maximum likelihood. to a countable set poses no problem. In the continuous case, we must work with intervals (or measurable sets) rather than point values. For any

to a countable set poses no problem. In the continuous case, we must work with intervals (or measurable sets) rather than point values. For any  be the maximum likelihood probability. If we consider an interval

be the maximum likelihood probability. If we consider an interval  as our maximum likelihood set, then the maximum likelihood “value” is the (measurable) set

as our maximum likelihood set, then the maximum likelihood “value” is the (measurable) set  . For any

. For any  for

for  . However, for a fixed

. However, for a fixed  . Put another way, we cannot simply assume uniform convergence.

. Put another way, we cannot simply assume uniform convergence. update. In that case, we keep the original prior and view the posterior as the aforementioned pruned version of the prior.

update. In that case, we keep the original prior and view the posterior as the aforementioned pruned version of the prior. .

. ‘s. All others are irrelevant. The maximum likelihood values typically form a tiny subset of

‘s. All others are irrelevant. The maximum likelihood values typically form a tiny subset of  unconstrained fantasy teams, ultimately evaluating under

unconstrained fantasy teams, ultimately evaluating under  million plausible teams and executing in under

million plausible teams and executing in under  seconds on a relatively modest desktop computer.

seconds on a relatively modest desktop computer.  players from one position and

players from one position and  each from

each from  players on a team, with specified positions P,P,C,1B,2B,3B,SS,OF,OF,OF. Salary cap is $50K. Constraints: (1)

players on a team, with specified positions P,P,C,1B,2B,3B,SS,OF,OF,OF. Salary cap is $50K. Constraints: (1)  hitters (non-P players) from a given real team, and (2) players from

hitters (non-P players) from a given real team, and (2) players from  different real games must be present.

different real games must be present.

players, with no position requirements. Salary cap is $50K. Constraints: (1) players from

players, with no position requirements. Salary cap is $50K. Constraints: (1) players from  hitters from any one team.

hitters from any one team.

hitters (non-P players) from a given real team, and (2) players from

hitters (non-P players) from a given real team, and (2) players from  players, with 2 pitchers and 5 hitters. Salary cap is $50K. Constraints are: (1)

players, with 2 pitchers and 5 hitters. Salary cap is $50K. Constraints are: (1)  players, with 2 pitchers and 6 hitters. $50K salary cap. Constraints are: (1)

players, with 2 pitchers and 6 hitters. $50K salary cap. Constraints are: (1)  such teams (for some

such teams (for some  hitter per team constraints fit this mold.

hitter per team constraints fit this mold.

denotes player

denotes player  in our listing.

in our listing.

of games represented in the given tournament. This would be all the games played on a given day. Almost every team plays each day of the season, so this is around 15 games. We’ll ignore the 2nd game of doubleheaders for our purposes (so a given team and player plays at most once on a given day).

of games represented in the given tournament. This would be all the games played on a given day. Almost every team plays each day of the season, so this is around 15 games. We’ll ignore the 2nd game of doubleheaders for our purposes (so a given team and player plays at most once on a given day).

of teams represented in the given tournament. This would be all 30 teams.

of teams represented in the given tournament. This would be all 30 teams.

of length

of length  of length

of length  of length

of length  of length

of length  of length

of length  of length

of length  if player

if player  if a pitcher, where

if a pitcher, where  , the teams from

, the teams from  , and the positions from

, and the positions from  . We’ll assign

. We’ll assign  . The vectors

. The vectors

groups (the positions), and marked as a partition.

groups (the positions), and marked as a partition.

groups (the teams), and marked as a partition.

groups (the teams), and marked as a partition.

groups (the games), and marked as a partition.

groups (the games), and marked as a partition.

groups (the teams for hitters plus a single group of all pitchers), and marked as a partition.

groups (the teams for hitters plus a single group of all pitchers), and marked as a partition.

(i.e. P,P,C,1B,2B,3B,SS,OF,OF,OF)

(i.e. P,P,C,1B,2B,3B,SS,OF,OF,OF)

(i.e.

(i.e.  )

)

(i.e.

(i.e.  (i.e.

(i.e.  (i.e.

(i.e.  )

)

items in any one group of Feature 4. (i.e.

items in any one group of Feature 4. (i.e.  . For a given group, we do this as follows. Assume that we are required to select

. For a given group, we do this as follows. Assume that we are required to select  and value

and value

then we cull item

then we cull item  groups with (

groups with ( ,

, ,

, ,

, ) allowed items. We need to select

) allowed items. We need to select  items from amongst these. In reality, fantasy baseball tournaments with flex groups have fewer other groups — so the size isn’t quite this big. But for other Fantasy Sports it can be.

items from amongst these. In reality, fantasy baseball tournaments with flex groups have fewer other groups — so the size isn’t quite this big. But for other Fantasy Sports it can be.  . Suppose we can prune just 1/3 of the players (evenly, so 30 becomes 20, 60 becomes 40, and 90 becomes 60). This reduces the state space by 130x to around

. Suppose we can prune just 1/3 of the players (evenly, so 30 becomes 20, 60 becomes 40, and 90 becomes 60). This reduces the state space by 130x to around  . If we can prune 1/2 the players, we reduce it by

. If we can prune 1/2 the players, we reduce it by  to around

to around  . And if we can prune it by 2/3 (which actually is not as uncommon as one would imagine, especially if many items have

. And if we can prune it by 2/3 (which actually is not as uncommon as one would imagine, especially if many items have  to a somewhat less unmanageable starting point of

to a somewhat less unmanageable starting point of  .

.  operations (it doesn’t), where

operations (it doesn’t), where  which is

which is  operations. In reality it would be far lower. So a careful cull is well worth it!

operations. In reality it would be far lower. So a careful cull is well worth it! . If it is set too high, we will cull too few items and waste time down the road. If it is too low, we may run into problems meeting the ancillary constraints.

. If it is set too high, we will cull too few items and waste time down the road. If it is too low, we may run into problems meeting the ancillary constraints.  and cost

and cost  in order to cull an item with value

in order to cull an item with value  to reflect this. If

to reflect this. If  is the number of selected items for group

is the number of selected items for group  strictly better items. Note that

strictly better items. Note that  is the total number of items in the

is the total number of items in the  group. Some of the same items may be available to multiple groups, but our collection must consist of distinct items. So there are

group. Some of the same items may be available to multiple groups, but our collection must consist of distinct items. So there are  possible selections. We can precompute this easily enough.

possible selections. We can precompute this easily enough.

. I.e. the product of the total combinations of this group and those that come after.

. I.e. the product of the total combinations of this group and those that come after.

is the sum of the top

is the sum of the top  is

is  . I.e., the best total value we can get from all subsequent groups.

. I.e., the best total value we can get from all subsequent groups.

is the sum of the bottom

is the sum of the bottom  is

is  . I.e., the cheapest we can do for all subsequent groups, if value is no concern.

. I.e., the cheapest we can do for all subsequent groups, if value is no concern.

) or from most to fewest (high to low

) or from most to fewest (high to low  ). We also are given

). We also are given  , the lowest collection value we will consider. We’ll discuss how this is obtained shortly.

, the lowest collection value we will consider. We’ll discuss how this is obtained shortly.  sorted by value or by cost depending on our 2nd choice above. I.e., we are iterating over the possible selections of

sorted by value or by cost depending on our 2nd choice above. I.e., we are iterating over the possible selections of  is the minimum cost of all remaining groups (

is the minimum cost of all remaining groups ( onward). This is the lowest cost we possibly could achieve for subsequent groups. It is the pre-computed

onward). This is the lowest cost we possibly could achieve for subsequent groups. It is the pre-computed  is the maximum value of all remaining groups (

is the maximum value of all remaining groups ( is the cost of our current selection for group

is the cost of our current selection for group  is the value of our current selection for group

is the value of our current selection for group  then there is no way to select from the remaining groups and meet the cost cap. Worse, all remaining iterations within group

then there is no way to select from the remaining groups and meet the cost cap. Worse, all remaining iterations within group  then there is no way to select a high enough value collection from the remaining groups. However, it is possible that other iterations may do so (since we’re iterating by cost, not value). We prune just the current selection, and move on to the next combo in group

then there is no way to select a high enough value collection from the remaining groups. However, it is possible that other iterations may do so (since we’re iterating by cost, not value). We prune just the current selection, and move on to the next combo in group  and value

and value  and group

and group  . We need to maintain a value-sorted list of our top collections in a queue-like structure.

. We need to maintain a value-sorted list of our top collections in a queue-like structure.  , the best value realized, This also resets

, the best value realized, This also resets  for some user-defined tolerance

for some user-defined tolerance ![{\epsilon\in [0,\infty]}](https://s0.wp.com/latex.php?latex=%7B%5Cepsilon%5Cin+%5B0%2C%5Cinfty%5D%7D&bg=fefeeb&fg=000000&s=0&c=20201002) ?

?

we report back (or do we keep them all)?

we report back (or do we keep them all)?

![{\delta\in [0,1]}](https://s0.wp.com/latex.php?latex=%7B%5Cdelta%5Cin+%5B0%2C1%5D%7D&bg=fefeeb&fg=000000&s=0&c=20201002) ?

?

or

or  will do. As mentioned,

will do. As mentioned,  . There is good reason to believe that, for any common tournament structure, the results would be consistent once established. It also is likely they will reflect these. Why? The fastest option allows the most aggressive pruning early in the process. That’s why so few collections needed to be analyzed.

. There is good reason to believe that, for any common tournament structure, the results would be consistent once established. It also is likely they will reflect these. Why? The fastest option allows the most aggressive pruning early in the process. That’s why so few collections needed to be analyzed.